by Darryl Miller Founder | AislePoint Consulting Independent grocery retailers are operating in one of the most competitive environments in the history of food retail. Customers today have more choices, while retailers face increasing pressure from inflation, labor shortages, rising operating expenses, aging infrastructure and changing consumer expectations. In this environment, one reality has become […]

Category: National

Posted inGrocery Research, Featured News, Meat/Seafood/Poultry, National, News

Survey: 55 Percent Of Consumers Are Buying Less Beef

Fifty-five percent of U.S. consumers are buying less beef or have stopped entirely amid rising prices, the New World screwworm outbreak and global trade disruptions, according to the 2026 Consumer Grocery and Protein Trends survey released July 21 by Blue Yonder. At the same time, one-third of consumers have increased their overall protein purchases in […]

Posted inProduce News, Association News, National, News

IFPA Calls For Stronger Traceability As Cyclospora Outbreak Grows

IFPA is calling for end-to-end traceability and stronger FDA food safety programs as the 2026 Cyclospora outbreak grows and a lettuce recall reaches retail shelves.

Posted inMeat/Seafood/Poultry, National, News, West

Pacific Seafood, Ocean Beauty Seafoods Merge Distribution Businesses

Pacific Seafood and Ocean Beauty Seafoods have merged their distribution businesses, combining two family-owned seafood companies across six western facilities.

Posted inWholesaler/Distributor News, Associations, Featured News, National, News

All ROFDA Wholesalers Now Have Joint FMI Membership

Retailer Owned Food Distributors & Associates members Affiliated Foods, AG Northeast, Certco and Piggly Wiggly Alabama Distributing Company have joined the FMI – The Food Industry Association. With these additions, all of ROFDA’s current wholesaler members now are FMI members. Associated Food Stores, Associated Grocers Baton Rouge, Associated Wholesale Grocers, Brookshire Bros. and URM Stores […]

Posted inAssociation News, Featured News, Independent Store News, National, News

NGA Asks NJ Gov. To Amend Fair Price Protection Act Before Signing

The National Grocers Association is urging New Jersey Gov. Mikie Sherrill to make “targeted, common-sense changes” to the Fair Price Protection Act (A4085) before signing it into law. In a July 17 letter to Sherrill, NGA outlined revisions it says would preserve the bill’s consumer transparency goals while avoiding unintended consequences for independent grocers. The […]

Posted inGrocery Research, Featured News, National, News, Online Grocery Technology

Delivery Leads As Online Grocery Growing Again, Coresight Finds

Online grocery shopping returned to growth in 2026, with 56.3 percent of U.S. consumers purchasing groceries online in the past 12 months, up from 53.6 percent in 2025, according to Coresight Research‘s ninth annual US Online Grocery Survey. The increase reverses two consecutive years of decline, and 58.7 percent of respondents said they expect to […]

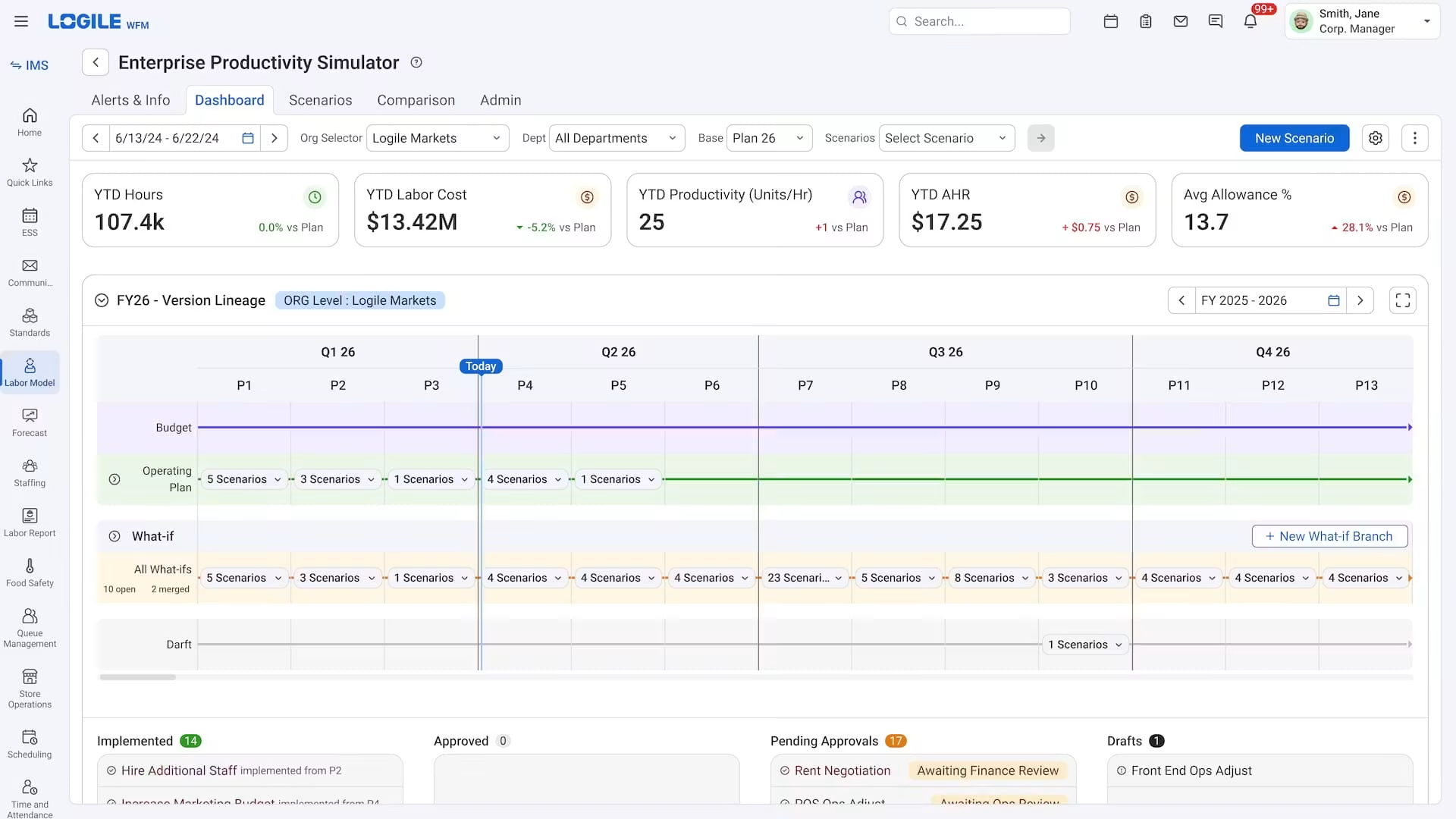

Posted inOnline Grocery Technology, Finance News, National

Logile Launches Enterprise Productivity Simulator For Retail Workforce Planning

Logile has launched its Enterprise Productivity Simulator, letting retailers model workforce and operational decisions across an entire chain before execution begins.