Retailers have many systems in place to track, study and audit nearly everything about a store, including inventory, sales and marketing efforts. But the cash office and front end are often an afterthought, tacked on to audits of other parts of the store. Audits of the cash office and the front end, including surveys of cashiers, self-checkouts, safes, customer service employees and bookkeepers, provide corporate with invaluable insight into how money is being handled.

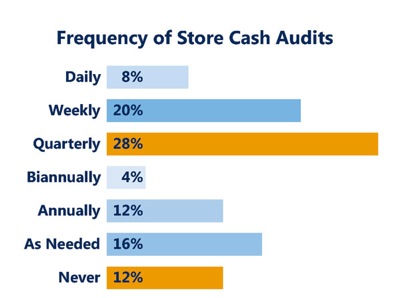

A recent grocery retail payment study, jointly sponsored by Balance Innovations and the National Grocers Association (NGA)*, revealed that practices regarding store cash audits vary widely. While 12 percent of the companies surveyed never conduct store cash audits, 20 percent do them weekly, 28 percent quarterly and 16 percent as needed. Larger companies reported a higher frequency of audits.

For smaller retailers, employee theft can occur when familiarity breeds trust, which unfortunately can be mislaid. Bookkeepers are often longtime employees who are trusted implicitly. For large retailers, employee theft can simply be too difficult to pinpoint across a large number of stores. Manual procedures and reports only make it easier for employees to manipulate the systems in place.

Rule No. 1:

Employ the element of surprise.

Many stores schedule their cash office audits along with audits of other areas like inventory. Knowing an auditor is coming allows employees to hide their activities. Unexpected surveys of cash office and front- end activities give corporate staff the chance to discover inaccuracies and address them as needed. Surprise audits also demonstrate an organization’s cash controls to employees.

“If you are tight on your cash controls, you’re tight on your other controls as well,” said Dr. Read Hayes, director of the Loss Prevention Research Council. “This maintains discipline, deters issues and communicates to your employees that your store is under control.”

According to the Balance Innovations/NGA survey, among companies that do store cash audits with at least some regularity, 38 percent do surprise audits whereas 33 percent opt for a combination of surprise and scheduled.

Rule No. 2:

Check for procedural compliance.

Beyond looking for outright employee theft, auditors must also observe and analyze whether corporate-dictated procedures are being followed for transactions such as refunds, voids and paid in/paid out. Ongoing non-compliance with corporate procedure costs the company money and is much harder to address than individual instances of theft.

Bookkeepers and front-end associates often develop their own habits over time, and these habits can vary from store to store, making it more difficult to identify and correct them.

Observing how corporate procedures are actually put into practice also allows auditors to analyze whether the procedures make sense for the company or if changes are needed.

Rule No. 3:

Automate procedures.

Manual procedures and reports provide many opportunities for employees to steal or make unintentional errors, both of which take away from the retailer’s bottom line.

Using automated tools creates transparency in which cash office and front-end transactions are tracked and logged, making it harder for employees to hide missing money or items from auditors. Automation can also enforce compliance with corporate procedures, eliminating paper reports that are easy to falsify. Store employees are no longer able to perform tasks “their way” and skip important tasks that safeguard the retailer.

This guest column by Janette Davis appears in the June print editions of The Shelby Report. Davis formerly worked in retail auditing and is VP of account management for Balance Innovations, a provider of cash management and reconciliation software solutions for retailers of all types and sizes.

*For the Balance Innovations/National Grocers Association Grocery Retailing Payments Study 2013, data was compiled from a three-page questionnaire sent to NGA membership and additional grocery retailing and wholesaling companies. Results were based on 26 grocery retailing companies, representing more than 2,600 stores; fielded January-March 2013. Data analysis conducted by 210 Analytics.