(Editor’s note: This is the second in a three-part series covering the release of the annual Power of Meat report. Part three will appear Friday.)

While meat continues to be a popular choice among shoppers, at 74 percent, some are not quite sure that meat belongs in a healthy and balanced diet, according to Anne-Marie Roerink, principal of 210 Analytics and presenter of the 17th annual Power of Meat report.

FMI – The Food Industry Association and the North American Meat Institute hosted an online presentation of the report March 8.

About one-third of those surveyed are trying to eat less meat and poultry. Contributing to this are shoppers’ ideas of healthy and ethical eating. This includes animal welfare, health, planet and social responsibility.

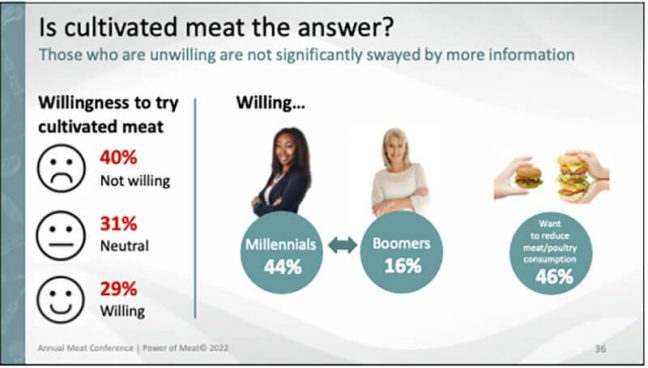

Among the meat alternatives available to consumers are cultivated meats and plant-based meats. About 40 percent of those surveyed said they are not willing to try cultivated meats, with 29 percent saying they would be willing to do so.

“This is an interesting area where I think we’re going to continue to see a lot of movement,” Roerink said.

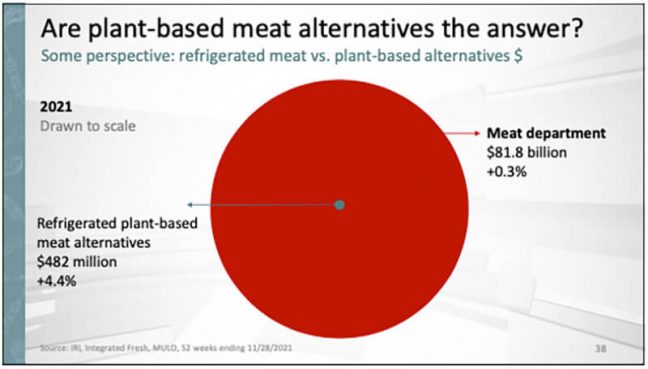

As far as plant-based meat alternatives go, where meat department sales were close to $82 billion in 2021, refrigerated meat alternatives were near half a billion dollars, up 4.4 percent, according to the report.

“What we saw really throughout 2021 is a decline, a deceleration of those growth rates and they actually started to go negative as of the third quarter in 2021,” Roerink said. “Now, we have to keep in mind they’re going up against very, very high growth rates the year before. We had an additional 28 percent in items the year before, whereas ’21 only benefited from about a 5 percent increase in items. So, it was really the same assortment that had to drive those increases.”

Also, plant-based meat alternatives didn’t have the inflation seen on the meat side and a greater share were sold on promotion. These are some of the reasons for the deceleration in growth rates, she said.

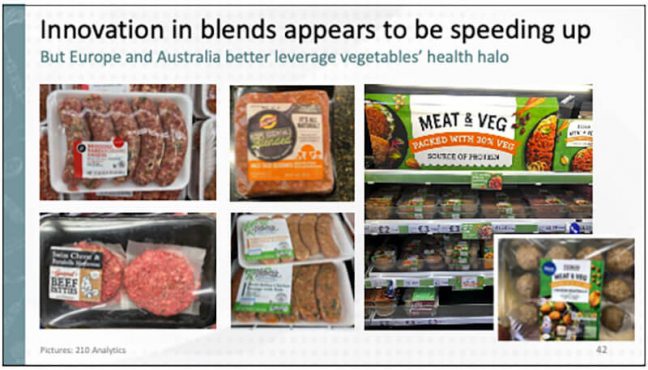

Blended items are appearing more often in stores and are becoming more popular.

“If we combine meat with vegetables or mushrooms, is that, then, the answer that people are looking for? We certainly see a greater number of people saying that they would occasionally or frequently try blended items,” Roerink said.

She said in years past she had to go to Europe, Australia and New Zealand to find good examples of blended items. But over the last few years, more U.S. grocers are coming up with “lots of innovations in the area of pork and beef and other proteins, mixed with a variety of mushrooms and vegetables,” Roerink said.

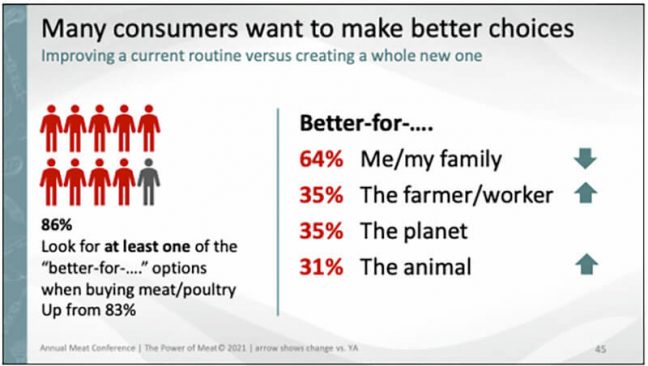

“What is really drawing the highest commitment from everybody – 63 percent of shoppers like to know about the who, what, where, when and how behind the meat and poultry they buy.” Roerink said she talks about transparency being the currency of trust, and the survey numbers show that, as 86 percent of consumers are looking for at least one “better for” option.

“That might be better for me, in other words, health, the farmer, the worker, the plant or the animal. And as you can see, we had a little bit of pressure there on nutrition, that one sat around 72 percent last year. And actually that’s social responsibility, the one that we never even looked at in years past until last year. It really drove that second slot and 35 percent looking for solutions in those areas,” she said.

Nutrition, portion control are considerations

Other ways shoppers are being mindful of healthy eating include being more aware of nutritional content and portion sizes. As an example, Roerink cited signage by Certified Angus talking about the various nutrients contained in the meat. An example out of England showed the number of calories, fat, saturated fat, salt and sugar and was color coded for an easy look to compare between bison and beef.

Portion control works well for bakery and for candy, according to Roerink. She included an example of a four-pack of sausage that can be ripped off one at a time.

“Of course, that’s something chicken has done for a long time, with the multiple individual packages in their larger bag,” she said.

Claims-based continuing to grow

The claims-based meat sector is at nearly $10 billion. This was a 2 percent increase in dollars, according to IRI numbers. However, there was some volume pressure, according to Roerink.

“And if we think about it, that makes all the sense in the world,” he said. “Because in 2020, we got meat from wherever we could get meat – if it was grass fed, it was grass fed; if it was organic, it was organic. So we are going up against a massive spike in claims-based meat. It’s probably not all that surprising to see that we’re not quite able to make that same volume. But certainly continued growth, especially in organic – the one area where we did see growth in both dollars and volume.”

Consumers continue to look for more production claims. These include “better for” qualities such as no added hormones, no antibiotics, all natural and grass fed. Organic is becoming more a niche area, Roerink said, with regenerative agriculture in there as well.

She also noted the importance of making sure people can understand industry jargon and production claims when they are used.

“My big lesson here is, if we use claims, let’s make sure that the consumers know what they mean and know why they are an actual advantage and worthy of a price differential,” Roerink said.

Meat counter

Last year, many shoppers said case-ready meat is as good as meat cut and created in store. This year, the report shows that 77 percent of shoppers have access to a meat counter.

Fifty-nine percent of shoppers, whether they have a meat counter or don’t have one, say they are glad they have a meat counter or wish that their store had one. That number is down.

“We’re seeing that idea of a meat counter [as a good thing] slide down a little bit. And of course, with all the labor issues that we’re having, it becomes a very interesting area for study,” Roerink said. “We look at the self-service meat case purchases – we see 32 percent buying exclusively from the self-service case, and 75 percent is the average share.”

Branded meat

Going back to 2010, branded meat has been a big influencer. According to the report, 75 percent said they have no brand preference when buying fresh meat and 63 percent said they had no brand preference when buying processed meat.

“Those numbers are down tremendously, for 40 in fresh and 29 in process, and what we saw this year is really an even greater focus on private brand, hand in hand with manufacturer,” Roerink said. “Private brand tends to be popular during those periods of high inflation. And the manufacturer brands have become really, really strong in those areas of specialty claims as well.”

The Power of Meat study was conducted by 210 Analytics on behalf of FMI – The Food Industry Association and the Meat Institute’s Foundation for Meat and Poultry Research and Education.