Walmart has detailed its back-to-school program for the 2026 season, offering what it describes as its lowest prices since 2019 on the 14 most popular school supplies found on classroom lists across the country, with select items starting at 25 cents. The retailer said it is offering more than 1,300 additional Rollbacks compared with last […]

Category: Walmart

Walmart, founded in 1962 by Sam Walton in Rogers, Arkansas, started with a focus on offering affordable goods to rural areas. Through the years the company has grown into a reliable retailer that has a deep connection with many citizens throughout the U.S.

The retailer prides itself on caring for its customers in store, and beyond their shopping experience. An example of this is the store sharing its parking lots with travelers and RV owners. Many Walmart locations allow free overnight parking for RVs, earning the title ‘Walmart Campers.’ As of 2023, the company boasts a staggering presence with over 4,700 locations across multiple states in the U.S.

Renowned for its extensive selection of products ranging from groceries to electronics and beyond, the brand caters to a broad spectrum of consumer needs. The retail giant’s commitment to providing competitive pricing and convenience resonates with shoppers seeking value and variety. Walmart continues to innovate and adapt, embracing technological advancements while maintaining its core principle of offering everyday low prices to its customers.

Posted inMerchandising News, News, Southwest, Walmart

Walmart, Sam’s Club Roll Back Prices On Thousands Of Summer Items

Bentonville, Arkansas-based Walmart has lowered prices on thousands of items through Walmart’s Rollbacks and Sam’s Club offers. “Customers count on Walmart to deliver the value they need every day, and summer is no exception,” said Julie Barber, EVP and chief merchant of Walmart U.S. “This summer, we’re making even more investments in price, with thousands […]

Posted inSustainability News, Midwest, Walmart

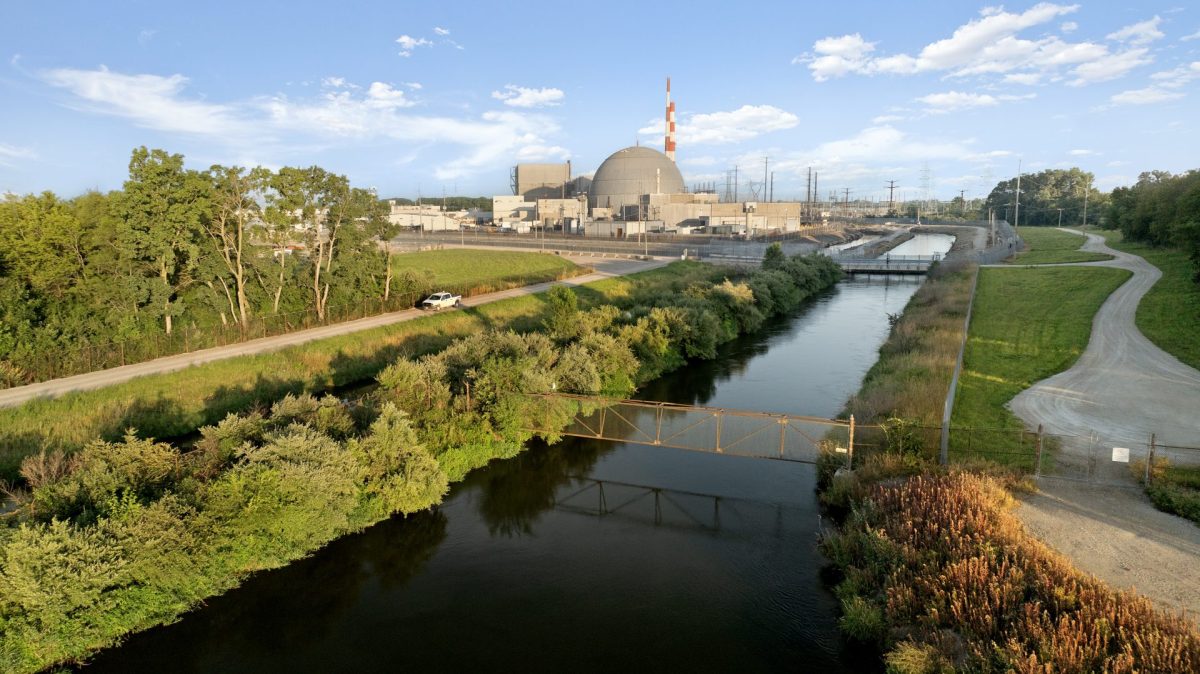

Walmart, Constellation Sign Nuclear Power Purchase Deal In IL

Walmart and Constellation have announced a long-term nuclear power purchase agreement for emissions-free electricity from Constellation’s Dresden Clean Energy Center in Illinois. The agreement includes about 176 MW of wholesale supply, including 30 MW of expanded generating capacity, and marks Walmart‘s first nuclear PPA – among the first of its kind between a large retailer and […]

Posted inOnline Grocery Technology, News, Southwest, Walmart

Walmart Acquires Vibe.co To Expand Self-Serve Connected TV Ad Platform

Walmart has entered into an agreement to acquire Vibe.co, a self‑serve connected TV (CTV) advertising platform designed to simplify advertising for small and mid‑sized businesses (SMB) and mid‑market brands. The acquisition advances Walmart’s strategy to build more accessible, full‑funnel advertising solutions through Walmart Connect, its commerce media business. By combining Vibe.co’s self‑serve CTV platform with Walmart’s commerce audiences, […]

Posted inBeverage News, Corporate Store News, News, Southeast, Walmart

Walmart, Dunkin’ Celebrate 150th In-Store Location In Oakwood, GA

Walmart has opened its 150th Dunkin’ restaurant inside a Walmart store at 3875 Mundy Mill Road in Oakwood, Georgia.

Posted inCorporate Store News, News, Southwest, Walmart

Walmart, P&G Commit $10.8M To Expand M25M Disaster Response Fleet

Walmart has provided a $10.8 million philanthropic investment in Matthew 25: Ministries (M25M) to expand a national disaster response fleet in collaboration with Procter & Gamble. The expansion aims to position relief vehicles within an eight‑hour drive of 90 percent of the mainland U.S. The funding will add seven laundry trailers and multi‑service shower units […]

Posted inOnline Grocery Technology, Corporate Store News, News, Southwest, Walmart

Walmart Completes 1M Drone Deliveries Across The U.S.

Bentonville, Arkansas-based Walmart has completed more than one million drone deliveries to hundreds of thousands of customers, a milestone the retailer announced May 29. What started as a pilot program a few years ago has expanded to 66 stores in four states serving five metro markets. Walmart said the service is designed for everyday “uh‑oh” […]

Posted inCorporate Store News, Featured News, News, Southwest, Walmart

Walmart Brings 30-Minute-Or-Less Delivery To 33 U.S. Markets

Bentonville, Arkansas-based Walmart is expanding its ultra‑fast delivery capabilities, bringing 30‑minute‑or‑less delivery to 33 U.S. markets. In the first quarter of 2026, Walmart completed millions of deliveries in 30 minutes or less to more than 19,000 zip codes across the country. The service is available in Austin, Dallas, Denver, Houston, Chicago, St. Louis, Atlanta, Tampa, […]